This article is an excerpt from the Shortform book guide to "Your Money or Your Life" by Vicki Robin and Joe Dominguez. Shortform has the world's best summaries and analyses of books you should be reading.

Like this article? Sign up for a free trial here .

Are you charting your monthly investment income? Have you projected your crossover point to know when you might reach financial freedom?

Getting a handle on your monthly investment income and crossover point are key aspects of achieving financial independence. In this article, you’ll learn the two steps of charting your investment income and discover how to project your crossover point.

Read more to get the details.

Visualizing Your Monthly Investment Income

Follow these two steps to chart your monthly investment income:

1. Calculate how much monthly investment income your capital will generate per month with the same formula discussed above: monthly investment income = capital x current long-term interest rate divided by 12. For current long-term interest rate, use the interest rate for 30-year US Treasury Bonds, or the interest rate for certificates of deposit.

This isn’t how much investment income you have at the moment you calculate it. It’s a projection of the monthly investment income you can expect if you invest your capital, regardless of the method you use to invest it.

Example: You have $1,000 in capital and the current interest rate is 4%. Plugged into the formula, you’d get $1,000 x 4% divided by 12 = $3.33 per month

This capital, if you invested it now, would conservatively yield $3.33 per month in compound interest, or $40 per year. Using a third color, plot $3.33 on your graph. Over time, as you build your capital each month, your graph will look something like this:

2. Apply this formula to your total savings each month. For example, if you save $500 next month, plug $1,500 into the formula.

Projecting Your Crossover Point

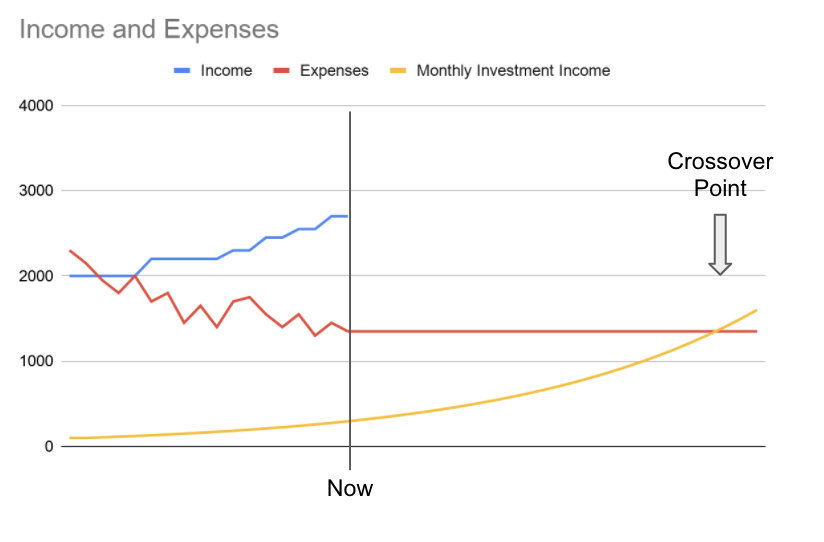

As your expenses stabilize, and your monthly investment income grows, you’ll be able to project your crossover point—approximately when you’ll reach financial independence.

To estimate your crossover point, you need several pieces of information:

- average yearly spending

- monthly withdrawal rate—the percentage of assets you’ll withdraw each month.

- total assets—how much money you’d need to make paid work optional.

Four percent is widely considered a safe withdrawal rate to avoid overdrawing your assets. Effectively, you need 25 times your annual expenses in order to guarantee a 4 percent per month withdrawal rate indefinitely. Use the following equation: total assets needed = average yearly spending x 12 divided by the withdrawal rate.

Example: You spend an average of $36,000 per year, or $3,000 per month. You want to be able to withdraw 4% of your assets per month. The formula would read: total assets needed = $36,000 x 12 divided by 4% = $900,000.00

In graph form, your monthly investment income line will have risen above your monthly spending line, as shown below:

When you track your monthly investment income, you’ll have a better handle on your crossover point. This is key to striving toward financial independence.

———End of Preview———

Like what you just read? Read the rest of the world's best book summary and analysis of Vicki Robin and Joe Dominguez's "Your Money or Your Life" at Shortform .

Here's what you'll find in our full Your Money or Your Life summary :

- The 9 steps to reach financial independence

- How to change your entire relationship with money and live a more meaningful life

- How to align your spending habits with your values, purpose, and dreams