This article is an excerpt from the Shortform summary of "The Big Short" by Michael Lewis. Shortform has the world's best summaries of books you should be reading.

Like this article? Sign up for a free trial here .

Maybe you’ve heard of mortgage-backed securities in relation to the 2008 financial crisis. But what are mortgage-backed securities? How do they differ from other investments?

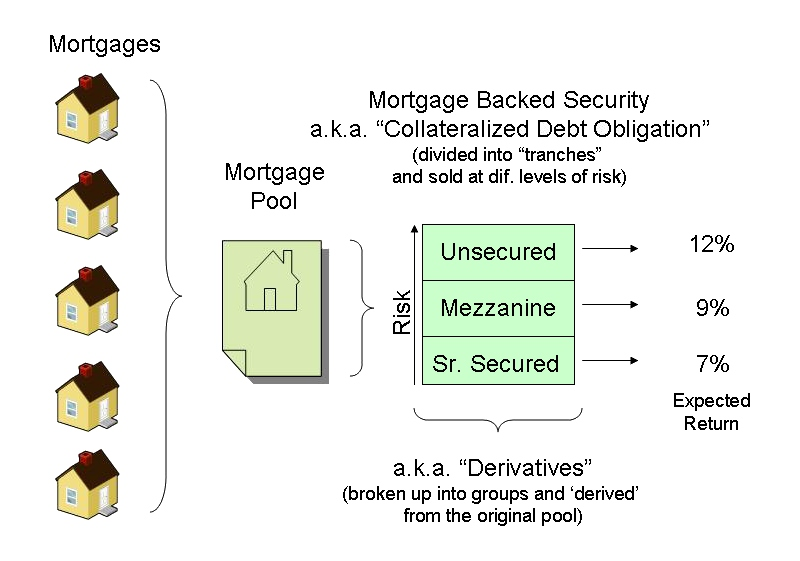

A mortgage-backed security (MBS) is essentially a bond, or debt instrument, that’s comprised of a bundle of home mortgages (often running into the thousands) that have been packaged together into a tradable asset.

Learn the history of mortgage-backed securities and how they infiltrated Wall Street, becoming one of the main contributors to the 2008 financial crisis.

An Untapped Asset—The Home

The deadly virus that infected the global financial system in 2008 was a relatively new class of asset: the mortgage-backed security. What are mortgage-backed securities? You can think of mortgage-backed securities as bonds, debt instruments. But these new securities were very different from a traditional bond that might be issued by a government or a corporation. These latter types of bonds were essentially loans, for which the lender would be paid a fixed interest rate over a given period of time until the bond matured and the bondholder received the principal (or “face value” as it’s sometimes known).

Traditional bonds always entailed some level of risk (the company or government from which you purchased your bonds could default, or fall behind on; payment or interest rates could rise and erode the value of your bond on the open market), but these risks were relatively transparent and easy-to-understand for most investors. This was not to be the case with mortgage-backed securities.

What Are Mortgage-Backed Securities?

Mortgage-backed securities brought the world of high finance into the lives of everyday Americans—even if they had no idea how much their homes had become chips on the table in the vast casino of global finance. A mortgage-backed security was made up of a bundle of home mortgages (often running into the thousands) that had been packaged together into a tradable asset. When an investor purchased one, she was purchasing the cash flows from the individual home mortgages that made up the security.

Mortgage-backed securities had actually existed for decades before the global financial meltdown of 2008, though few investors (and even fewer ordinary people) had heard of them. For most of the 1980s and 1990s, the mortgage-backed security (MBS) market was an obscure corner of the overall bond market, drawing only occasional interest from major financial institutions like Morgan Stanley, Bearn Stearns, and Goldman Sachs.

The Problem with Traditional Mortgage-Backed Securities

Many investors at this time, in fact, shied away from mortgage-backed securities because the cash flows were undesirable. During this era, the mortgage-backed bonds were made up of rock-solid mortgages to creditworthy homeowners who were in little risk of default. Ironically, this was the original problem that investors had with these securities. Borrowers could always pay off their mortgages any time they wished, and it was usually easiest for them to do so in a low-interest environment.

Buyers of mortgage-backed securities at this time weren’t concerned about default: they were worried about being paid back too quickly. As an investor, you want to be sitting on cash when interest rates are high so that you can reinvest that money and earn even greater returns. The basic nature of mortgage-backed securities seemed to cut against this basic investing principle. Because people were paying off their mortgages when interest rates were low, the holder of a mortgage-backed security received their money back precisely when it was least valuable to them.

Making Mortgage-Backed Securities More Appealing

Wall Street, however, had a workaround to this problem. Instead of buying the whole bundle, investors could purchase a slice of the underlying mortgages (or “tranche” as they would become infamously known). Investors in the lowest tranche would receive the first wave of repayments (again, when this cash influx was least valuable). To compensate for the untimely cash flow, these investors would receive a higher interest rate from the bank on the tranche that they purchased. Investors in the highest tranche, or level, received the lowest rate of interest but enjoyed the security of knowing that they would be getting their money back at the time when it was worth the most.

Mortgage-Backed Securities and the 2008 Financial Crisis

But this whole structure created a perverse incentive: mortgages made to un-creditworthy borrowers could actually be worth more than mortgages made to qualified borrowers. Lenders had the incentive to lend to people who would couldn’t pay their mortgages when interest was low. This led to a high number of defaults. Because of these subprime mortgages, mortgage securitization set the stage for the 2008 financial crisis.

In summary, what are mortgage-backed securities? They’re bonds created from bundles of home loans, and because they’re worth more when people don’t pay off their mortgages quickly, they led to a dramatic increase in loans to un-creditworthy borrowers and contributed to the 2008 financial crisis.

———End of Preview———

Like what you just read? Read the rest of the world's best summary of "The Big Short" at Shortform . Learn the book's critical concepts in 20 minutes or less .

Here's what you'll find in our full The Big Short summary :

- How the world's biggest banks contributed to the 2008 financial crisis, greedily and stupidly

- How a group of contrarian traders foresaw the bubble popping, and made millions from their bets

- What we learned from the 2008 crisis - if anything